Table of Contents...

- Facing the Threat of Repossession in South Wales

- How the Repossession Process Works in the UK

- What Repossession Does to Your Credit Rating

- Why Estate Agents Are Too Slow to Help

- How a Fast Auction Sale Can Prevent Repossession

- The Auction Timeline: Instruction to Completion

- What Your Property Could Achieve at Auction

- Fast, Confidential Marketing That Gets Results

- Case Study: Repossession Avoided in South Wales

- Final Thoughts: Act Now, Before It Is Too Late

Facing the Threat of Repossession in South Wales

Receiving a default notice from your mortgage lender is one of the most unsettling experiences a homeowner can go through. The formal language, the deadlines, the growing weight of arrears — it can feel as though the situation is moving faster than your ability to respond, and that the options available to you are narrowing by the day. I want to say clearly at the outset of this guide: you are not alone, and you almost certainly have more choices than you realise right now. The most important thing you can do is take action early, because the earlier you act, the more control you retain over the outcome.

At The Property Auction House, I have worked with homeowners across South Wales who were facing exactly the kind of financial pressure you may be experiencing — missed payments, court hearings scheduled, and the very real prospect of losing their home. In many of these cases, a fast voluntary sale through property auction allowed them to clear their mortgage, protect their credit rating, and move forward with their lives from a far stronger position than an enforced repossession would have left them in. The key in every case was the same: they reached out early enough for us to be able to help.

In this guide, I will explain how the repossession process works, what a completed repossession means for your credit file and future borrowing, why traditional estate agents are rarely fast enough to help in these situations, and how a well-run online auction sale can give you the speed and legal certainty you need to take back control. If you are based in Swansea, Neath Port Talbot, Bridgend, Llanelli, or anywhere across South Wales, this guide is for you.

How the Repossession Process Works in the UK

It is important to understand that a lender cannot simply repossess your home the moment you miss a payment. There is a legal process that must be followed, and understanding each stage of that process gives you a clear picture of where you stand and — critically — how much time you realistically have to act. Most mortgage lenders will make contact after two or three missed payments and attempt to agree a repayment arrangement before taking any formal action. A formal default notice is typically issued after three to six missed payments, and this must give you at least 14 days to remedy the arrears before the lender can take further steps.

If the default notice is not remedied, the lender can apply to the court for a possession order. This triggers a court hearing at which you have the right to attend and present your circumstances. Judges have discretion to adjourn or suspend possession orders where there is a realistic prospect of the arrears being resolved, including through a sale of the property. A suspended possession order means the lender cannot enforce possession provided you comply with any conditions attached — usually continuing to pay the current mortgage plus a contribution towards the arrears. If you breach those conditions, the lender can apply for a warrant of possession, at which point physical repossession becomes imminent. You can find comprehensive guidance on the full process at Citizens Advice.

The key practical point is that there are usually several months between a first missed payment and an actual repossession date — often six months to a year or more in practice, particularly if you engage actively with the court process. This window, if used correctly, gives you genuine time to explore a voluntary sale and potentially exit the situation with your credit rating protected and some equity preserved. Understanding where you are in this timeline is the essential starting point for making good decisions, and it is something I am always happy to walk through during a no-obligation valuation call.

What Repossession Does to Your Credit Rating

A completed repossession leaves a serious and lasting mark on your credit file. The mortgage account will show as in default, and the repossession itself is recorded for six years from the date it occurred. During this period, obtaining a new residential mortgage is extremely difficult — most high street lenders will decline an application outright once a repossession appears on the credit file, and specialist lenders who will consider it typically charge significantly higher interest rates to reflect the perceived risk. The financial consequences of a repossession extend well beyond the loss of the property itself, and they can affect your ability to rent privately, obtain a car on finance, and in some cases secure employment in roles that require financial background checks.

A voluntary sale before repossession proceedings complete can significantly limit this damage. If you sell your property and clear the outstanding mortgage balance from the proceeds before the court process results in a possession order being enforced, the default may still be recorded on your credit file, but the repossession itself does not take place. Future mortgage lenders distinguish between an account that fell into arrears but was resolved through a voluntary sale, and one that ended in a court-ordered possession — and that distinction matters greatly when you come to apply to borrow again in the future. Some lenders will consider applications from borrowers who had a historical default resolved through a voluntary sale within a relatively short window — a route that is simply not available to those who went through the full repossession process.

There is also the issue of a potential shortfall debt. When a lender repossesses and sells a property, their priority is recovering the outstanding debt — not achieving the best possible price on your behalf. Repossessed properties sold through lender-instructed processes frequently achieve below-market values, and if the sale proceeds do not cover the full mortgage balance including arrears, legal costs, and the lender’s fees, the lender can pursue you personally for the difference. That shortfall debt can follow you for years and has its own negative impact on your credit profile. A voluntary sale that you manage yourself, with professional support, gives you the best realistic chance of clearing the debt in full and protecting yourself from this additional liability.

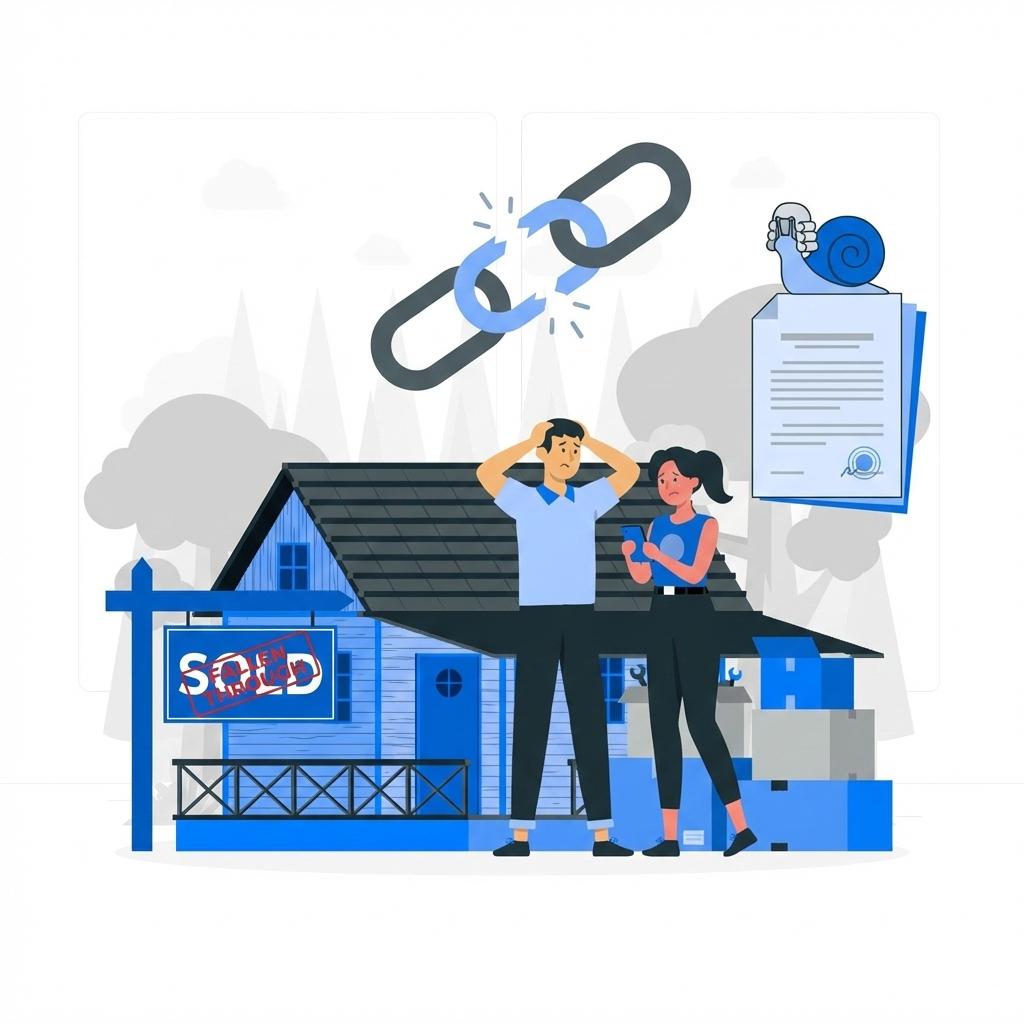

Why Estate Agents Are Too Slow to Help

The instinct when you need to sell quickly is often to contact a local estate agent — they are visible, familiar, and most people have some experience of how they work. The fundamental problem is that a traditional estate agency sale takes, on average, around six months from instruction to completion in the current market. For a homeowner facing a possession hearing scheduled in six to eight weeks, that timeline is simply not compatible with the urgency of their situation. A standard estate agency listing will not save you from repossession unless you started the process many months ago, and by the time most people contact us, that window has already closed.

Estate agents also operate on an open-ended timeline with no fixed completion point. They list your property, arrange viewings, receive offers, and then wait for a buyer to secure a mortgage and progress through a lengthy conveyancing chain. Each stage introduces the potential for delay — buyers who withdraw after a survey, mortgage applications that are declined, chains that collapse when an onward purchase falls through. Even a straightforward sale regularly takes three to four months from accepted offer to completion. When your lender has a court date approaching and your credit rating is on the line, this unpredictable, open-ended process is not a solution — it is a false hope that consumes precious weeks you cannot afford to lose.

There is also a subtler problem. Estate agents who are aware that you are selling under financial pressure may inadvertently signal your circumstances to buyers, inviting low offers from people who recognise your vulnerability. A well-run auction sale, by contrast, creates a level playing field where multiple buyers compete against each other simultaneously, with no individual buyer aware of your personal situation. That competitive dynamic — not your private circumstances — is what drives the final price, and it consistently produces fairer results than a private negotiation where a single buyer knows you have limited time and no alternatives.

How a Fast Auction Sale Can Prevent Repossession

An online auction sale at The Property Auction House moves on a fundamentally different timeline to a standard estate agency listing, and it is specifically this timeline that makes it the most effective option for sellers facing repossession. From the moment you contact us, we can typically have your property valued, the legal pack instructed, and the property live on our platform within one to two weeks. The marketing period runs for three to four weeks, and when the auction closes, contracts exchange immediately and the winning buyer pays a 10% deposit within 24 hours. That is a legally binding, unconditional exchange — not subject to survey, not subject to finance, not subject to anything. If you need a fast, certain sale in Swansea or across South Wales, this is the process that delivers it.

In practical terms, from first contact to legally binding exchange, the process typically completes in five to six weeks. Completion of the sale then follows 28 days after exchange, meaning the full process from first call to funds in your account can take as little as nine to ten weeks. For context, the average estate agency sale in England and Wales currently takes around six months from instruction to completion. In a situation where every week matters and your lender is watching the clock, this compression of the timeline is not a minor convenience — it is the difference between protecting your credit and losing it.

A legally binding exchange of contracts is also the most powerful tool you have in any negotiation with your mortgage lender. When you can present your lender with written confirmation that your property has exchanged at auction, that the deposit has been received, and that completion is contractually scheduled within 28 days, the conversation with your lender changes entirely. Most lenders will pause or postpone repossession proceedings when they can see that a sale is not merely in progress but legally committed. That confirmation of exchange is something only auction can deliver at this speed, and it is consistently the most effective way to demonstrate to a lender that the situation is genuinely under control.

The Auction Timeline: Instruction to Completion

Let me walk through the timeline in practical terms so you can assess whether it fits your situation. The first step is a free, no-obligation valuation, which I can usually arrange within 24 to 48 hours of your initial call. During this visit, I will give you an honest assessment of your property’s likely auction value, explain the guide and reserve price structure clearly, and walk you through every stage of the process. There is no pressure and no cost at this stage — just clear, straight-talking advice from someone who understands both the auction process and the emotional weight of the situation you are in.

Once you decide to proceed, your solicitor prepares the legal pack — typically within one to two weeks, depending on how readily the title documents are available. Simultaneously, we photograph and list the property across our own platform, Zoopla, and PrimeLocation. The marketing period runs for three to four weeks, during which registered buyers can view the property, review the legal pack, and prepare their bids. At the close of the auction, if a reserve-meeting bid has been placed, contracts exchange immediately. The winning buyer pays their 10% deposit within 24 hours, and formal completion of the purchase takes place 28 days later. For more information about how the full process works, visit our property auctioneers Wales page.

The total timeline from first contact to completion is typically nine to eleven weeks, though in urgent situations we can sometimes work with solicitors to expedite legal pack preparation and compress the timeline further. Even at the standard pace, nine weeks is a fraction of what a traditional estate agency sale takes, and it offers something the estate agency route fundamentally cannot: a fixed, contractually binding completion date from the moment the auction closes. That certainty — the knowledge that the sale will complete on a specific date and that nothing can unravel it in the meantime — is exactly what sellers in repossession situations need most.

What Your Property Could Achieve at Auction

One of the most persistent concerns I hear from sellers facing repossession is that they will have to accept a heavily discounted price in order to sell quickly. This is an understandable worry, and it is one that the reputation of traditional closed-bid auction rooms has perhaps reinforced. The reality of a well-run online property auction in today’s market is quite different. Our buyer database includes hundreds of active investors and developers across South Wales who are competing for good residential properties, and that competitive dynamic frequently drives prices significantly above the guide. Properties in well-located areas of Neath Port Talbot, Bridgend, Swansea, and Llanelli regularly achieve results that represent genuinely fair value for sellers in a tight timeframe.

The guide price we set for your property is a carefully researched marketing figure designed to attract maximum buyer interest and stimulate competitive bidding. It is not a ceiling, and it is not our expectation of the final result — it is the opening figure from which competitive bidding starts. Our valuation process takes into account the current condition of the property, comparable recent sales in the local area, and the realistic level of investor demand at the time of marketing. We set a confidential reserve price together during the valuation — the minimum figure you have agreed the property will not be sold below — and this gives you a guaranteed floor while leaving full room for competitive bidding above it.

I always encourage sellers in this situation to assess the auction price relative to their specific objective, rather than comparing it to a theoretical maximum that a six-month open market campaign might or might not have produced. If your objective is to clear your outstanding mortgage balance, protect your credit rating, and move forward quickly, the relevant question is not whether the auction price equals an aspirational ceiling but whether it achieves the outcome you actually need. In the vast majority of cases, the answer is yes — and in a timeframe that gives you back control before it is taken from you.

Fast, Confidential Marketing That Gets Results

We understand that sellers facing financial difficulty do not always wish to broadcast the reason for their sale to neighbours, family members, or local contacts. Our marketing approach is designed to present your property accurately and attractively on its merits, without disclosing your personal circumstances. Every listing we produce highlights the property’s key features — its location, size, condition, and potential — in language that speaks to the active buyer market. The urgency of your situation is never reflected in the marketing materials, and the buyers who bid on your property will do so based on the commercial case for the asset, not on any knowledge of why you are selling.

Every property we list is professionally photographed and described in detail, then published simultaneously across our own website, Zoopla, and PrimeLocation. This gives your property maximum exposure across the full breadth of the active buyer market in South Wales and beyond. We also send targeted notifications directly to the buyers on our database who have registered an interest in properties of your type and in your area. These are not casual browsers — they are active, qualified buyers with funds available, and many of them will be in a position to bid within days of receiving a notification. This direct outreach is what consistently generates competitive interest from the first week of marketing, and it is one of the most significant advantages we offer over any other method of sale.

We manage all viewings on your behalf, coordinate access with you directly, and handle all buyer enquiries throughout the marketing period. You do not need to be present for viewings and you do not need to deal with calls from unqualified enquirers. Our team provides you with regular updates so you always know exactly how much genuine interest your property is attracting ahead of the auction date. From first instruction through to the fall of the hammer, the entire process is managed professionally, promptly, and with full awareness of the sensitivity of your situation.

Case Study: Repossession Avoided in South Wales

Let me share an example that illustrates how the process can work in practice. Earlier this year I was contacted by a homeowner in the Neath Port Talbot area who had fallen into mortgage arrears following a period of serious illness and a significant reduction in household income. By the time he called us, he had missed five mortgage payments, received a default notice from his lender, and had a possession hearing scheduled for the following month. He had spoken to a local estate agent who had suggested that a sale would take three to four months at a minimum — a timeline that would see the court proceedings complete long before the property could be sold voluntarily.

We visited within 48 hours, set a guide price that we were confident would attract strong investor interest, and had the property live on our platform within a week of instruction. During the marketing period, three registered buyers from our database booked viewings and two of them submitted pre-auction expressions of interest. On auction day, competitive bidding pushed the final price above the guide. Contracts exchanged immediately at the close of the auction, and the deposit was received within 24 hours. Completion took place 28 days later — two weeks before the possession hearing was due to take place.

The proceeds were sufficient to clear the outstanding mortgage balance in full, including all arrears, with a modest amount of equity returned to the seller. His solicitor was able to provide the lender with written confirmation of exchange within days of the auction closing, and the lender agreed to withdraw the possession application pending completion. He avoided a county court judgment, avoided a repossession entry on his credit file, and was able to plan his next steps from a position of resolution rather than ongoing crisis. From our first conversation to completion, the entire process took nine weeks.

Final Thoughts: Act Now, Before It Is Too Late

If you are reading this guide because you are in mortgage arrears, have received a default notice, or are worried that you are falling behind and cannot see a realistic way to catch up, the single most important message I want you to take away is this: act now, and act early. The earlier you take control of the situation, the more options you have available to you. A voluntary sale on your own terms is always preferable to an enforced repossession organised by your lender, and the difference in outcome — for your credit rating, your equity, and your long-term financial wellbeing — can be significant and lasting. Every week of inaction is a week in which options narrow further.

Auction is not a method of last resort for people in desperate circumstances. It is a professional, efficient method of sale that puts you back in control and gives you the fastest realistic route to a legally binding transaction at a fair price. The buyers we work with are experienced professionals who assess properties on their commercial merits and bid competitively when they see good value. Your situation may feel urgent and overwhelming, but from the perspective of an investor buyer, your property is simply an asset in a location they understand, at a price that makes commercial sense. That framing — placing the focus back on the property and away from the circumstances — is what a good auction consistently delivers.

If you would like to understand what your property could realistically achieve and whether a fast auction sale can help you avoid repossession, I would genuinely welcome that conversation. Enter your postcode below for a free, no-obligation valuation, and I will personally assess your property, give you an honest guide price, and walk you through every step of the process in plain English. There are no upfront fees, no pressure, and absolutely no obligation — just straightforward, practical advice from someone who has been helping South Wales homeowners navigate difficult situations successfully for over 20 years.

Office Address

42 Mansel Street, Swansea, SA1 5SW